Finance, Management Accounting and Relevant Theoretical Approaches

This section covers:

- Linkages between demographic information and health service information - its public health interpretation and relationship to financial costs

- Budgetary preparation, financial allocation and service commissioning

- Methods for audit of health care spending

Allocation of Funds to the NHS - National Level

In 2007/08, the NHS in England will spend some £93 billion. Almost all of this expenditure is financed from general taxation (either general taxes from the 'Consolidated Fund' or from National Insurance contributions - see Table 1).

|

Source of Funds |

% Health expenditure |

|

Consolidated Fund Expenditure |

73.9 |

|

National Insurance Contributions |

20.2 |

|

Trust interest receipts / loan repayments |

3.3 |

|

Charges and miscellaneous income |

2.5 |

|

Capital receipts |

0.1 |

Table 1: Sources of NHS Expenditure, England 2005/06

In England, the overall total tax funding allocated to the NHS (excluding the minor sources of income detailed in Table 1) is decided politically, via the mechanism of HM Treasury's three-year budget allocation to the Department of Health (DH). Every three years, a Comprehensive Spending Review (CSR) assesses the competing spending forecasts and priorities of all spending departments across the public sector, and relates these to the overall priorities of the Government of the day. At the conclusion of the CSR process, each department of state receives a three-year 'settlement' (i.e. indicative budgets for the next three years). While scope exists to allocate additional (or, indeed, reduced) funding to a department at each annual Budget within the three-year CSR period, such adjustments tend to be kept to a minimum.

In Scotland, Wales and Northern Ireland, the overall allocation of tax funding to the NHS is decided by the respective devolved government. Westminster allocates an overall budget (covering all functions of each devolved administration) to each of the Scottish, Welsh and Northern Ireland Assembly Governments. Each devolved administration then makes its own relative prioritisation of spending decisions across its own key areas of responsibility (e.g. health, social care, education etc.). The overall total allocation of funds to Scotland, Wales and Northern Ireland is influenced by the 'Barnett Formula'. The Barnett Formula works to ensure that, when spending in England on a particular programme increases, the total allocation to the devolved administrations receive an increase equivalent to that in England for the comparable programme, given their population share. The Barnett Formula thus relates only to increases in expenditure in England; it is not a 'needs-based' formula, and does not calculate the overall funding allocated to each devolved administration. It is also used to determine the appropriate funding contribution of the three devolved administrations to UK-wide bodies (e.g. the National Patient Safety Agency). Once they have received their global budget, each devolved government is at liberty to allocate it as they see fit across any of their spending responsibilities.

Allocation of Funds to the Local NHS

Most funding for the NHS in England flows via Primary Care Trusts (PCT), who contract with and pay the ultimate providers of NHS care. The allocation of funds from the DH at national level to each local PCT is undertaken via the resource allocation formula, which seeks to ensure an equitable distribution of funding given differing population needs between PCTs. This general approach dates back to 1976, when the Resource Allocation Working Party (RAWP) report recommended distribution according to two fundamental criteria:

(1) adjustments to be made for perceived differences in the need for health care; and

(2) account to be taken of the unavoidable differences in costs of providing services.

The underlying objective of RAWP was to ensure funding to provide equal opportunity of access to health care for people at equal risk. The key factor used to measure need was Standardised Mortality Ratio (SMR) - utilisation was rejected because of the supposed strong influence of service provision (i.e. supply). The RAWP approach remained in operation in England until 2002, when a wide-ranging review (the 'AREA' review) sought to upgrade the resource allocation formula to account not only for differences in needs for health care, but also to contribute to the reduction of avoidable inequalities in health status between populations. This review incorporated several new variables, including certain morbidity measures, and remains in operation today.

The current formula (a 'weighted capitation' formula) is used to calculate each PCT's target share of the total resources available to the NHS, to provide a unified allocation for funding local NHS services. The formula includes factors for local population size, drivers of need (age, sex, and various other proxies for need), and regional cost variations (the 'Market Forces Factor'). The formula is currently under review by the Advisory Committee on Resource Allocation, which aims to improve the performance of the formula, in particular by accounting more effectively for unmet need.

In Scotland, a broadly analogous approach to weighted capitation funding has been in place since 2000. The 'Arbuthnott Formula' uses population, age-sex cost weights, additional needs factors and 'unavoidable costs of excess supply' factors to derive weighted capitation funding for each Health Board. The NHS Scotland Resource Allocation Committee (NRAC) reported in September 2007 with a set of recommendations to improve and refine the Arbuthnott Formula, to account for new data now available and (as in England) to address unmet need more effectively.

In Northern Ireland, each Health and Social Services Board receives a block grant based on the Regional Capitation Formula (calculated on population size, age, sex, and deprivation and rurality factors). A review of the contents of this formula is currently under way.

In Wales, by contrast, funds have been allocated from Cardiff to health boards largely on the basis of historical 'cost plus' budgeting since devolution, without using a weighted capitation formula. However, moves are currently under way to develop a 'Direct Needs' formula.

Readers should therefore note that, at the time of writing, reviews of NHS funding formulae are under way in each of the four home countries.

There are, of course, some elements of NHS funding which fall outside the basic funding formula from national to local NHS levels in each administration; however - especially in England - considerable effort has been expended to minimise the scope of funds flowing via different mechanisms. For example, 'Choosing Health' funds previously allocated as ring-fenced monies for PCTs are now incorporated within the unified allocation. Certain non-recurrent allocations remain separate; the largest of these are for the National Specialised Commissioning Advisory Group's budget for specialised services, the Agenda for Change supplement, GP premises development, and development of Child and Adolescent Mental Health Services. However these amount to only 2% of PCTs' total allocations.

Flow of Funds from NHS Commissioners to Providers

This section describes in more detail the basic mechanisms by which funds flow from NHS commissioners (PCTs and practice based commissioners) to health care providers in the key areas of primary care, secondary care and specialised services. It focuses on England; arrangements in the other three home countries are substantially different from each other.

Primary Care Services

Primary care services are the largest area of NHS activity when measured by patient contacts, and consume a substantial share of total NHS resources. Traditionally, primary care has been provided by General Practitioners, remunerated via a nationally negotiated contract for 'General Medical Services' (GMS). Under national GMS terms and conditions, individual GPs and practices hold a contract with a PCT, and the PCT pays GPs from its unified allocation. A number of alternative mechanisms for funding primary care services have been introduced in recent years:

-

Personal Medical Services (PMS)

-

Alternate Provider Medical Services (APMS)

-

Primary Care Trust Medical Services (PCTMS)

However, GMS remains the vehicle by which the great majority of primary care services are funded. A far-reaching reform of the GMS GP contract was implemented in 2004; in 2006/07 the GMS contract was revised under the terms of the partnership arrangement between the NHS Confederation and General Practitioners Committee of the British Medical Association, to allow for more flexibility for GP primary care delivery.

General Medical Services (GMS)

GMS contracts remunerate GP's under these key headings

-

Global Sum Payments - a capitation payment based on the practice's registered population

-

Minimum Practice Income Guarantee - a sum designed to protect historic (pre-2004) income levels, progressively being phased out and replaced by the Global Sum payment

-

Quality & Outcomes Framework - described below

-

Directed Enhanced Services - covering improved access, choice and booking, practice based commissioning and promoting IM & T adoption across the NHS

-

Childhood Immunisations - payments for achieving pre-specified target coverage levels for child immunisations (for 2 and 5 year old immunisation schedules)

-

Payments for Specific Purposes - e.g. certain other immunisation programmes

-

Premises Development and IM&T - direct expenditure covered from a central budget - reviewed annually

-

Other, including dispensing doctors, maternity service provision etc.

Quality and Outcomes Framework

The Quality and Outcomes Framework (QOF) is the annual reward and incentive programme detailing GP practice achievement results. QOF is a voluntary process for all surgeries in England and was introduced as part of the GP contract in 2004.

QOF awards surgeries achievement points for:

-

managing some of the most common chronic diseases e.g. asthma, diabetes

-

how well the practice is organised

-

how patients view their experience at the surgery

-

the amount of extra services offered such as child health and maternity services

Good financial management is critical to ensuring that QOF is an accurate and targeted measure of GP productivity and costs in delivering services to patients at local level.

The QOF has been in operation since 2004, and is still developing and being refined, especially in the area of exception reporting where there are gaps in clinical information or insufficient measurable evidence to validate reporting.

The QOF aims to encourage appropriate and high quality clinical care in respect of key chronic diseases. Potentially, exception reporting could influence the level of financial reward to practices. This is a major concern to DH and as a reliable empirical measure, QOF is still some way from being totally accurate. There is still fierce debate about the viability of providing 'quality payments' to GP practices, for marginal improvements in health gains from improved workloads. There is a case for benchmarking QOF against other similar delivery methods, such as those from NHS Direct and star rating bonuses.

However, as a guideline tool for measurement of service delivery at local level, it is a considerably useful tool in allowing the measurement of spending at local level by Strategic Health Authorities (SHA) and NHS when planning for central budget allocations and longer term strategic planning.

Secondary and Specialised Care

Since 2002, the funding of secondary and specialised NHS care has shifted away from a model focussed on budgets for providers that were preset and based on overall estimates of likely activity. The DH set about introducing plans for fundamental changes to the way that fundeds flow through the NHS. In October 2002, DH issued a report - Reforming NHS Financial Flows - Introducing Payment by Results (PBR).

Its proposals included moving towards a nationally agreed set of prices, commissioning at specialty level based on volumes adjusted for case mix using Healthcare Resource Groups (HRG). Initially focusing on the commissioning of elective care between PCTs and NHS Trusts, it has since expanded to the broad church of primary care encapsulating all commissioning arrangements within the NHS since then. The objectives of this policy shift were as follows:

-

To pay NHS Trusts and other providers fairly and transparently for services delivered, while managing demand and risk

-

To support the introduction of patient choice by ensuring that diverse providers can be funded according to where patients choose to be treated

-

To reward efficiency and quality in providing services

-

To help match capacity to demand

-

To refocus discussion from disputes over price to the volume and mix of services that meet population need and the pathway of care for patients.

This involved moving from a local based tariff to a national tariff system by 2007, which has now been largely achieved.

Payment by Results - How does it work?

Under Payment by Results (PBR), hospitals are paid only if an operation or treatment is carried out. The Department of Health has drawn up a long list of procedures, such as hip replacements or treatment for heart attacks, each with its own HRG code. There are more than 1,000 HRG codes, designed to capture all the treatments and procedures that a patient might have while in hospital for a particular condition or operation.

Effects of PBR applications

PBR means a hospital will be paid the fixed price for every treatment it undertakes. This drives high cost NHS Trusts towards cost efficiencies.

Efficient hospitals can keep the extra money, just as businesses retain their profits.

The assumption underlying this new system is that hospitals will want to make a surplus, on top of their existing legal obligation to balance the books. To do this, they will have to retain existing patients and attract new ones. This includes diverting patients away from other hospitals or places of treatment, by being 'more responsive' to their needs. In other words, only a few years on from the publication of the NHS Plan, competition between hospitals is now being planned into the system.

The recent introduction of the Polyclinics concept in early 2008 is a further extension of competitive service deliveries now cascading down towards GP surgeries and triage style units. The intention is to treat as many patients as possible, even when it would be more appropriate for treatment to take place elsewhere. However, it may also encourage local primary care trusts to work with general practices to improve care and reduce the risk of costly hospital admissions

What is the speed of PBR implementation?

90% of hospital care is targeted to be covered by this PBR framework by 2009, according to latest DH estimates.

Advantages and Disadvantages of PBR

Advantages include:

-

Greater efficiency and productivity

-

More transparency

-

Clearer accountability to the tax payer

Disadvantages include:

-

Rewards volume, not results

-

Quality of Care possibly compromised

-

Tariff management manipulation, especially for harder to price treatments

-

Not a 'one size fits all' tool i.e. mental health treatments for complex conditions such as bi-polar disorder, are hard to price using a national tariff system

-

Silo hospitals - specialist hospitals become more prevalent, rather than general hospitals, forcing patients into difficult treatment choices and decisions - patient care could be compromised.

A recent report from the Audit Commission (February 2008) has assessed the first four years of PBR implementation, and concludes that PBR has increased the transparency and fairness of the payment system; it has contributed - along with other policies - to improvements in activity and efficiency in elective care; and it has not led to any reduction in quality (a negative outcome some critics had predicted).

What methodologies are used to measure PBR?

Core to this financial remodelling of NHS financial management, is the creation of Service Level Agreements (SLA). SLA's are the core working documents, encapsulating use of Prince 2 project management principles combined with established private sector accounting practices, and is the working contractual document that ensure financial flows work, that activity requirements are understood and that arrangements for risk sharing and monitoring activity are understood and agreed.

SLA's comprise of these key elements

-

Activity and Resources

-

Service Developments/Changes

-

Quality Standards

-

Information Flows

-

Monitoring

-

Risk Sharing and Management

-

Handling In-year Variances

-

Incentives, Rewards and Penalties

-

Arbitration

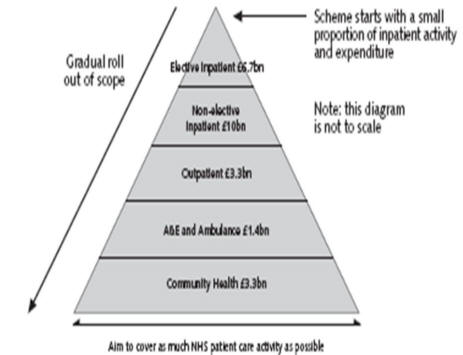

How the scope of financial flows developed from 2002 - 2007

Back in 2002, the initial DH focus on elective surgery represents only a small amount of total NHS spend on patient activity. The DH aims to cover as much of patient activity as possible.

The above uses 2000-1 HCHS figures to illustrate the scope of NHS activity accounting for almost £25bn NHS expenditure (excludes general practitioners, dental, pharmacy, drugs). DH has extended the scope of the scheme to provide enhanced/additional GP services.

Source: Department of Health - Reforming NHS Financial Flows - October 2002

Evolving Health Care Financial Management

As a direct result of this overhaul of financial reporting within the NHS, Service Line Reporting (SLR) followed on from the PBR initiative. SLR aims at PCT's and Foundation Trusts.

What is SLR?

SLR is standard practice in well run private sector companies. SLR helps foundation trusts and NHS trusts develop a better understanding of operational and financial performance of their various services and hence improve strategic and clinical decision-making. The benefits include:

-

enhanced financial transparency and accountability;

-

improved clinical engagement in performance management and operational leadership;

-

increased quality and productivity;

-

increased strategic insight; and

-

greater ability to quickly assess both profitable and loss making areas within trusts.

Why Service Lines?

In business terms, the service line is the natural 'business unit' of the hospital - a distinct unit with identifiable customers, products, revenues and costs that is run as an independent business with its own income and expenditure. Managing service-lines well enables effective delegation of accountability to a unit of a size and scale that is manageable for developing strategy and driving performance.

Why is SLR important?

As a private sector tool, SLR brings cost and performance efficiencies to businesses in a real-time manner, and flexibly allows business to respond to changing market forces. In NHS trusts SLR measures a trust's profitability by each of its service-lines, rather than just at an aggregated level for the whole trust. While NHS trusts focus on the management of overall profitability of the whole trust, at service line level most trusts have continued to monitor cost, income, activity and use of resources separately. This has prevented clinicians and managers from understanding the overall actual profitability of their service, what drives profitability, or what impact different decisions have on profitability.

What benefits does SLR bring?

SLR enables a trust to increase its productivity by providing board members, clinical leaders and managers with the necessary financial information to:

-

Make informed decisions, for example, on how to manage an existing portfolio of services, prioritise new service developments or plan new clinical investments.

-

Manage performance on an annual and monthly basis against agreed levels of financial performance at the service-line level

Why is SLR important in future financial planning?

DH has indicated that it will use reliable SLR data to help inform future tariff setting. This means that those trusts that can demonstrate accurate costing data are likely to be in a strong position to influence future PBR income streams.

Monitor, the Independent Regulator of Foundation Trusts says SLR can deliver measurable outcome improvements within a short timeframe, and that delivery of clinical support at all levels can be influenced, modified and improved on an ongoing real time basis.

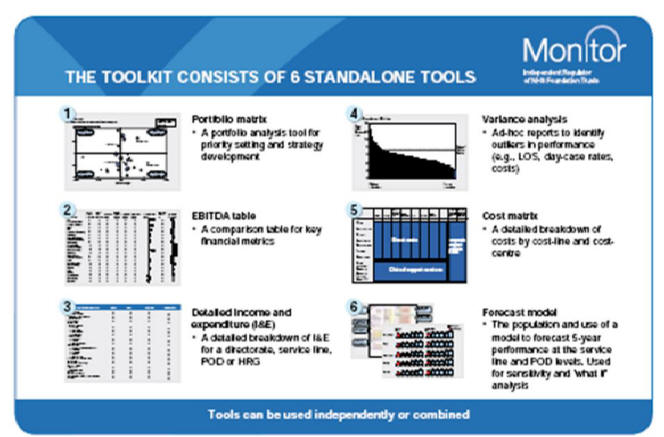

The SLR model revolves around a 'toolkit' of six key reporting tool measurements which span across the entire workings of a trust. This toolkit is illustrated below.

Source: Monitor - December 2006 Ho How Service-Line Reporting can

The toolkit enables Trusts to monitor EBITDA as a pure financial performance indicator whilst comparing this to deliverables, within the overall scope of the portfolio matrix, which allows for strategic and goal/task set objectives to be examined and measured on an ongoing basis.

Indicators used in SLR

This is not an exhaustive list, but for a typical trust can include

-

financial performance

-

demand

-

clinical standards

-

patient care outcomes (even drilled down to individual patient level),

-

training

-

sickness

-

staff turnover

SLR for 'Lean Thinking'

Often the phrase in the private sector used for efficient companies is operating 'lean and mean'. Lean thinking is a more sympathetic but effective measurement outcome in the NHS by improving the value of services and eliminating waste. This is achieved when decisions are taken by those able to identify what really matters to patients and for staff delivering a service. Resources can be more effectively deployed, with more therapeutic activities, a better ward environment, and better models of clinical staffing.

Care Pathways

SLR can also aid the development of defined care pathways'. At St. Andrew's Healthcare, the largest mental health charity in the UK emphasis is placed on individual patients as they make progress through the pathway, from a higher dependency area on admission, moving through several wards toward discharge. The costs of each step in the pathway of care are transparent within the charity, which is able to set a meaningful tariff. In specialist areas of mental health and learning disability NHS commissioners have for some time been moving towards tariffs based on levels of ward security and patient dependency, with payment by results being more promising for definable outpatient treatment programmes. SLR works well as part of a wider programme of decentralisation, with devolution of responsibility for performance.

Budgeting

For the purposes of clarity, budgeting can be split into two distinct sections

Financial Budgeting - this is linked, at local operational level, to the performance of the trust on an ongoing basis.

Programme Budgeting - this is linked to the patient pathway concept instigated by the DH at the same time as the financial review process overhaul started in 2002.

Financial Budgeting

Financial Budgeting has evolved dramatically in the past few years, with a shift from line item management to a more holistic approach using the PBR and Service-Line reporting (SLR). Line item management in its simplest form was more of a micro managed method of examining spending in relation to outputs and did not practically link directly at the point of delivery. The result was slow and expensive process, and diminished value for money. There was often too much focus on the detail of saving costs without examining more practical outcome issues.

With PBR and SLR, under a SLA framework, trusts are now required to ensure that as part of its performance monitoring, it regularly links clinical and patient outcomes with financial performance.

The 1997 directive on investment appraisal criteria applies a discount rate of 6% for all investment decisions, in respect of new capital expenditure commitments and linking this to the ongoing financial performance of a Trust, primary care unit or GP practice, This is a modest investment based return on capital compared with the private sector, where double digit returns on capital are commonplace.

On costs

It should be noted that, when considering staff costs, a variety of factors in addition to headline salary must be taken into account. These factors include the employer contribution to National Insurance (NI) and pension arrangements, and the various other infrastructural costs associated with the provision of employment. Together, these are called 'on costs' and are generally factored in at between 28% and 100% in addition to the overall salary. The percentage will vary by institution and what they include. For example if only the NI and pension costs are included this is in the region of 26-30%, but more realistically other costs have to be added in, including: desk space, telephone, sickness, holiday, training as well as other department costs to maintain the infrastructure of the business e.g. finance, HR etc

Performance

Below is how a typical Trust Finance Department would deliver this information to its Board for strategic and operational management purposes on a regular reporting cycle. The headings and tables below are not exhaustive but provide a guide to linking performance to tariffs, service level agreements and local SHA objectives.

There is usually an executive summary of highlights that is followed by the detail shown hereafter.

Income Performance

| Operational Budget £000 |

INCOME | Current Month | Year to Date | ||||

| Budget £000 |

Actual £000 |

Variance £000 |

Budget £000 |

Actual £000 |

Variance £000 |

||

| PCT SLAs Specialised Services Income Other Income for Patient Care Net Patient Care Income Debt Repayment Uncovered Risk Reserves Adjustments |

|||||||

| Sub Total Income | |||||||

| Interest Receivable | |||||||

| Total Income | |||||||

SLA Performance

PBR Performance to DD/MM/YY

| POD | Cumulative Activity | Cumulative Value | ||||

| Budget Spells |

Actual Spells |

Variance Spells |

Budget £000 |

Actual £000 |

Variance £000 |

|

| Elective Day Case Elective Inpatient |

||||||

| Total Elective | ||||||

| Non Elective | ||||||

| Outpatients 1 Outpatients FUP Outpatients Procedures |

||||||

| Total Outpatients | ||||||

| A&E | ||||||

| TOTAL | ||||||

Expenditure

| Operational Budget £000 |

EXPENDITURE | Current Month | Year to Date | ||||

| Budget £000 |

Actual £000 |

Variance £000 |

Budget £000 |

Actual £000 |

Variance £000 |

||

| Pay Pay Rebasing Reserve Non Pay Non Pay Rebasing Reserve Depreciation Recovery Plan |

|||||||

| TOTAL EXPENDITURE | |||||||

Risks

| Description of Significant Risks | (H)igh (M)edium or (L)ow |

Total Level of Risk £000 |

| Pathology Send Away Risks Theatre Sessions Increased demand for Cat A Training Removal Expenses Legal Fees Ad Hoc Maintenance Gas Price Rise Predictions Electricity Price Rise Predictions Teaching Contract Cost Risks Central Teaching Budgets |

Recovery Plan

Cash Position

Capital Commitments

Conclusion

Income and Expenditure Account For The Period Ending DD/MM/YY

| Operational Budget £000 |

INCOME | Current Month | Year to Date | ||||

| Budget £000 |

Actual £000 |

Variance £000 |

Budget £000 |

Actual £000 |

Variance £000 |

||

| PCT SLAs Specialised Services Income Other Income for Patient Care Net Patient Care Income Debt Repayment Uncovered Risk Reserves Adjustments |

|||||||

| Total Income |

|||||||

| EXPENDITURE

Pay |

|||||||

| TOTAL EXPENDITURE |

|||||||

| OPERATIONAL SURPLUS/(DEFICIT) |

|||||||

| Profit/(Loss) on Disposals | |||||||

| SURPLUS/(DEFICIT) BEFORE INTEREST |

|||||||

Interest Receivable Deficit Interest Charge Unwinding if Discount Trust Debt Remuneration Other Adjustments |

|||||||

| RETAINED SURPLUS/(DEFICIT) |

|||||||

The entire way in which the NHS is now accounting for its patients is along private sector lines, driven by performance, and geared to ensure that each operating unit works within its revenue budget allocations given to provide best practice, in a value for money way. PBR and SLR enable this functionality to be delivered.

Financial Allocation Options

Private Finance Initiative (PFI)

In addition to the various measurement methods used for managing budgets, the provision of capital has always been a source of much debate. Over the past 15 years, the Private Finance Initiative (PFI) has provided a ready source of capital infrastructure investment that was in the past Exchequer funded, but is now a risk and reward sharing mechanism between the public and private sectors.

PFI covers a variety of spending and capital raising requirements within what is called the Investment Life-Cycle.

Strategy and Planning

Outline Business Case (OBU)

Procurement

Full Business Case (FBU)

Implementation

Linked to PFI Projects, the Treasury is seeking to ensure that all capital expenditure on projects gives the taxpayer good value for money.

Value for Money and Discounting

Calculations of value for money compare the differences between public procurement where all the costs of hospital development are paid in the first few years and PFI where they are spread over 25 or 30 years. A discounted cash flow analysis is carried out to compare the 'buy now, pay later' principle. Discounting introduces an interest rate assumption. Discounting is widely used in the private sector as it is assumed to maximise value for shareholders. Its relevance to the public sector, where profit maximisation is not the objective of investment, is unclear. Discounting is applied to measure the cost of the value of future events to those in the present period, or in other words, comparing the benefits of 'value today against value tomorrow'.

The key fundamental issue is the relative value of £1 today versus £1 at some time in the future. There are several issues that impinge; interest rates, increasing uncertainty with increasing timescales and the relative effective value of currency from one time to another: known as 'purchasing power parity'.

Cost comparisons, once discounted, are expressed as net present costs. The option with the lowest net present cost is said to offer the best value for money. In practice, this single figure is the basis of approval. Value for money is assumed to provide neutral criticism, but discounting clearly favours private finance with its protracted repayment schedule.

The level at which the discount rate is set determines whether or not private finance option shows value for money. The higher the discount rate applied, the lower the value placed now on expenditure in later years. Treasury guidance imposes a discount rate of 6%, with the effect that £100 of expenditure incurred in five years' time has a 'present value' for appraisal purposes of £74.73, in 10 years of £55.84, in 20 years of £31.18, and so on. Note that for the purposes of appraisal, the costs to be discounted are expressed in real terms.

Discounted cash flow analysis

The table below shows a worked example of discounted flow analysis, with a discount rate of 6%. The result is that expenditure of £1000 in annual statement of £100 over 10 years, starting next year, is held to be equivalent to expenditure of £736 this year. This result depends entirely on the discount rate used - when a 4% discount rate is used, the figure is £811.

| Year | Total cash flow (£) | Discounted cash flow (£) |

| 0 | 0 | 0 |

| 1 | 100 | 94.34 |

| 2 | 100 | 98.00 |

| 3 | 100 | 83.96 |

| 4 | 100 | 79.21 |

| 5 | 100 | 74.73 |

| 6 | 100 | 70.50 |

| 7 | 100 | 66.51 |

| 8 | 100 | 62.74 |

| 9 | 100 | 59.19 |

| 10 | 100 | 55.84 |

| Total | 1000 | |

| Net present cost | 736.02 |

The discount assumption affects fundamentally the appraisal outcome.

Source: British Medical Journal, July 1999

Determining economic advantage

The 6% discount rate does not reflect interest rates on government borrowing, any more than NHS capital charges reflect the actual cost of public sector capital. The choice of 6% was a policy decision. According to Treasury guidance, 'the practical choice of 6%, from the top of the range ... is an operational judgement, reflecting, for example, concern to ensure that there is no inefficient bias against private sector supply.'

Source: HM Treasury The Green Book, HMSO London 1992.

The 6% discount rate favours private finance and obscures the central characteristic of private finance: the higher cost of capital. Therefore, economic appraisal assumes from the outset what it is held to prove: the economic advantage of private finance.

Key Summary Points to consider comparing PFI and Public Sector Funding

-

Investment under the private finance initiative can cost more than public sector procurement. The annual charge for the use of privately financed facilities is often between 9% and 18% of the original construction cost, whereas government can borrow at Public Works Loan Board interest rates of 3.0% to 3.5%. NB: These funds come from the issue of HM Government Bonds, known as Gilts.

-

The extra cost of private finance is often disguised (and sometimes confused) by the Treasury's requirement that NHS trusts discount costs at 6% per annum when comparing the costs of the private finance option with public sector investment

-

The amount of risk transferred to the private sector under privately financed deals is often exaggerated. PFI deals reduce the short term capital expenditure strain on the Exchequer but costs more in the long run in capital and interest costs to the taxpayer.

Five Case Model

Non health related businesses also use what is called the Five Case Model.

Strategic Fit

Economic Case (Viability)

Financial Case (Affordability)

Commercial Case

Management Case

When appraising large capital projects or large service delivery project undertakings, a thorough business case appraisal is needed to ensure that all contingency risks are covered financially and practically.

Use of the OGC DH Gateway and OGC successful delivery toolkit aids all procurers in sourcing capital in the correct and measurable format, including project management and project execution guidance, using PRINCE 2 as the foundation skill sets needed to implement effective delivery.

Certain capital expenditure is now recognised as not being served best by PFI. These specialist areas include:

-

Information Management and Technology (IM&T)

-

NHS LIFT (NHS Local Improvement Finance Trust)

NHS LIFT

NHS LIFT is a vehicle for improving and developing frontline primary and community care facilities. It allows PCT's often in conjunction with other agencies, to invest in new premises in new locations, and not merely reproduce existing types of service. It is flexible in the types of buildings it provides from one stop primary care centres, to GP premises, and community hospitals.

NHS LIFT does link the NHS with Local Authorities as the DH has a national joint venture with Partnerships UK through a company - Partnerships for Health (PHH).

Pros and Cons of NHS LIFT can be summarised thus

Pros

Flexibility, Scale and speed, Services Integration and Common approach

Cons

Time Commitment (25 year schemes), Cost of participation (over time) and Securing Agreement on usage (often competing partners have different usage agendas).

NHS LIFT compared to traditional PFI projects are better for shorter timescales, and reduced multi procurement needs, unlike larger valuer, slower delivered PFI projects.

There is a tightly prescribed format for business case approval processes, along the lines of non health related business procurement and evaluation methods of the Five Case Model.

Financial Disclosure

Financial information forms part of the overall DH requirements for an annual Statement of Internal Control (SIC), which has been in force in its present guise, since 2003/2004 where there has been only one template for the SIC, which all NHS bodies must sign (with the exception of certain Special Health Authorities i.e. The Information Centre, who are using the Treasury Government Department model).

The guidance from DH for the preparation of this SIC is shown below (headings only, unless of a financial nature, in which case the heading is expanded)

1. LEADERSHIP AND STRATEGY

There should be a risk management strategy.

2. BOARD ASSURANCE FRAMEWORKS

Board Assurance Frameworks should be embedded.

3. CONTEXT FOR RISK MANAGEMENT

The context in which risk has to be managed should be identified:

Identifying the context for risk management should incorporate consideration of Stakeholders, as appropriate to the organisation including:

patients;

public interests;

service user interests;

Ministers and the Department of Health;

wider societal interests;

risk aspects of relationships inside and outside of the NHS (including key suppliers of goods and services), to incorporate:

ways in which the behaviour of 'partners' affects the organisation;

ways in which the behaviour of the organisation affects the 'partners';

the risk priorities of 'partners.'

4. RISK IDENTIFICATION AND EVALUATION

Risk should be identified and evaluated in a structured way.

5. CRITERIA FOR EVALUATION OF RISK

There should be specific criteria for evaluating risk encompassing a range of factors.

5.1 Criteria for evaluating risk should give consideration to:

financial / value-for-money issues;

service delivery / quality of service issues;

reversibility or otherwise of realisation of the risk;

the quality or reliability of evidence surrounding the risk;

the impact of the risk on the organisation / stakeholders / partners /others;

defensibility of the realisation of the risk.

5.2 The criteria should be applied consistently and methodically across the whole range of risks.

6. RISK CONTROL MECHANISMS

Appropriate controls should be in place in relation to each risk:

7. REVIEW AND ASSURANCE MECHANISMS

Review and assurance mechanisms should be in place.

A pro-forma SIC format used by NHS bodies (headings only) is shown below covering these areas:

Scope of responsibility

The purpose of the system of internal control

Capacity to handle risk

The risk and control framework

Review of effectiveness

Programme Budgeting

Programme budgeting is simply a method of capturing past activity and expenditure into programmes of care, with a view to influencing and tracking activity and expenditure in those same programmes in the future. It is particularly relevant to commissioning and public health applications. The Programme Budgeting Project for England (with parallels in the other countries of the UK) has defined 23 medical programme budget categories to capture the totality of NHS expenditure in every PCT in practical, clinically relevant, objective-based groupings. The first 20 categories are based on the chapters in the International Classification of Diseases. The other three were added during exploratory work, to capture the rest.

Programme budgeting simplifies the big picture to a single spreadsheet and can help explain, co-ordinate, plan, communicate and stimulate change.

Here are some tips and guides on how best to use programme budgeting

-

look at your PCT's programme budget map and those of others in your cluster

-

pick programmes of interest or concern (perhaps where your PCT is an 'outlier')

-

unpick the detail in these programmes - discuss them and understand them

-

tap into the creativity of local clinicians, managers, public and partners - think of new ways of deploying those resources to improve health outcomes before you add or subtract from a programme as a whole

-

weigh up the added costs and added benefits (or reduced costs and lost benefits) if resources are used in new ways. Some changes, like redeploying staff, can be virtually cost-neutral

-

consult with others before acting - programme budgeting is an aid to thought not a substitute for it!

-

make decisions in public - programme budgeting is all about openness

-

make it happen - the art of management!

-

evaluate whether it delivered the outcomes, and cost what was assumed, in practice share what you learned - good or bad - we are all on a voyage of discovery.

Source: Health Service Review - December 2004

Extensive resources are available freely on the DH Programme Budgeting Project website:

http://www.dh.gov.uk/en/Managingyourorganisation

These resources include downloadable spreadsheets with programme budgeting and population data for each PCT, guidance and case studies, and presentations. The section on Annual Population Value Review provides an excellent introduction to using Programme Budgeting data to support local commissioning decisions. Programme Budgeting data are increasingly being used by researchers to investigate the empirical relationship between health spending and health care outcomes (see papers by Martin, Rice and Smith).

Other Useful Resources for Financial and Resource Planning

In addition to the DH Programme Budgeting site (see above for details), a number of other resources are likely to be of value to public health specialists working at local level on commissioning and resource planning issues.

Unit Costs of Care

The PSSRU produce an annual publication Unit Costs of Health and Social Care, which provides very useful unit costs for many types of health and social care service, available free at: http://www.pssru.ac.uk/uc/uc.htm

DH provides extensive detail on 'reference costs' (reported unit costs) for hospital and community health services. Reference costs are the basis for calculating PBR tariffs, but they are also extremely useful as a source for estimating costs of services and service changes. They are available at: http://www.dh.gov.uk/en/Publicationsandstatistics

Benchmarking Tools

The NHS Institute for Innovation and Improvement has developed a suite of productivity indicators (the Better Care, Better Value indicators) which provide a useful and user-friendly benchmarking tool with which to compare the efficiency of acute care trusts and PCTs. The 15 high-level indicators cover the domains of clinical productivity, finance, prescribing, procurement and workforce. They are available for use at: http://www.productivity.nhs.uk/default.aspx

Further Reading & References

- Audit Commission. February 2008. 'The right result? Payment by Results 2003-07.' www.audit-commission.gov.uk/reports/index.asp

- P. Brambleby, A. Jackson, J.A. Muir Gray. 2007. 'Better allocation for better health and healthcare: the first annual population value review'. http://www.dh.gov.uk/en/Managingyourorganisation

- Department of Health - Reforming NHS Financial Flows - Introducing Payment by Results - October 2002

- King's Fund - April 2005 - Payment by Results

- P Sugarman & J Watkins (2004).`Balancing the Scorecard: Key Performance Indicators in a Complex Healthcare Setting'. Clinician in Management 12, 129-32.

- P Sugarman (2007) `Governance and Innovation in mental health' (editorial) Psychiatric Bulletin 31: 283-285.

- R S Kaplan & D P Norton, The Balanced Scorecard (Harvard Business School Press Boston, 1996)

- J K Liker, The Toyota Way the company that invented lean production (McGraw-Hill, 2004)

- S. Martin, N. Rice, P. Smith. 2007. 'The link between health care spending and health outcomes: evidence from English programme budgeting data.' http://www.york.ac.uk/inst/che/pdf/rp24.pdf

- S. Martin, N. Rice, P. Smith. 2007. 'Further evidence on the link between health care spending and health outcomes.' http://www.york.ac.uk/inst/che/pdf/rp32.pdf

- `Trading Places', Healthcare Finance (Healthcare Financial Management Association, March 2007)

- How service-level reporting can improve the productivity and performance of NHS foundation trusts (Monitor Independent Regulator, December 2006)

- Daniel Jones and Alan Mitchell, Lean Thinking in the NHS (NHS Confederation)

- Guide to Developing Realisable Financial Data for Service-Line Reporting, Monitor, December 2006

- Toolkit for Presenting Service-Line Reporting Data, Monitor, December 2006

- Getting the most out of managing service lines: using service-line reporting in the annual planning process, Monitor, March 2007

- Getting the most out of service-line reporting: organisational change and incentive-based performance management, Monitor, March 2007

- Health Service Review 58, December 2004, Dr. Peter Brambleby

- Department of Health - Private Finance Initiative - www.dh.gov.uk

- PFI in the NHS - is there an economic case? Gaffney, Pollock, Price and Shaoul - British Medical Journal, July 1999

Department of Health, The Quality and Outcomes Framework Exception Reporting Statistics for England 2006/07 - published 30 October 2007

© M Deacon & M Hensher 2008